The Covid -19 pandemic is much more than a simple public health emergency. The rapid spread of infections across geographies have disrupted social, educational, political as well as economic activities. Among the many behavioural changes that the pandemic has brought about, some are social distancing, wearing of masks, avoiding handshakes as well as making contactless, online payments.

The pandemic has also driven home the importance of having a clean credit history and in maintaining your repayments on time, as far as possible. A clean financial track record is your gateway to getting credit and liquidity in times of need, and that is desirable in economically uncertain times.

So, given the mobility and social distancing restrictions imposed by the ongoing pandemic, how do you make non-cash, remote payments towards your TVS Credit loan account on time?

Let us show you several easy to use, online, contactless payment modes that you can use to preserve your health as well as your repayment track record!

1.Pay online through www.tvscredit.com

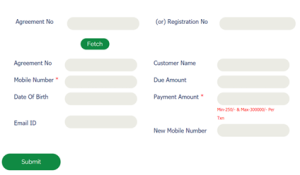

Visit the above mobile-friendly website, click on the click on the Pay Online link, and you will find the following screen:

Fill in the agreement number, or registration number, and the website will pull up your loan account details. Now all you have to do is enter the amount you wish to pay and click on the submit button. You can make the payment via your PAYTM, Airtel Payments Bank, Atom, Google Pay or UPI platforms.

Now make the payment according to your choice of platform. In each of these cases, all you pay is the actual amount, with no additional fees or surcharges.

1. Pay via our TVS Credit Saathi Mobile App

You can also download the TVS Credit Saathi App from Google Play Store to make online payments as well as to get bonus offers. The procedure for using the app is simple. Once you have opened the app, click on Pay Now, enter your loan registration number, select your preferred mode of payment and complete the transaction.

2. Pay Via the PayTM app:

In Paytm, search and select the option to make Loan EMI Payment, then choose TVS Credit as your lender, and enter your loan registration number and your mobile number to proceed. You can then opt for the payment mode of your convenience, from the options offered, and make your payment.

3. Pay Via WhatsApp

To do this, initiate a chat on our registered WhatsApp number- +91 6385172692. You will soon receive relevant instructions. Follow the instructions and select the desired mode of payment, and you can quickly complete the payment process.

4. Pay using Airtel Payments Bank

If you are one of those who have registered with Airtel Payments Bank, you can opt for this payment mode.

So, these are the five ways in which you can make safe and contactless payments towards your TVS Credit loan account. If you face any problems in using any of the above, do connect with us and we will be glad to assist you.

Meanwhile – stay safe, healthy and happy.